Succession Planning Tips for Transferring Business Ownership

Running a business is not just about reaching your goals today. It’s also about preparing for tomorrow. One of the biggest tests that a business can face is the transition from one leader to the next, especially when transferring ownership. Succession planning is a critical process, ensuring there’s a smooth handover of leadership. Let’s dive into some practical tips to help you plan for a successful transition.

Understand the Importance of Early Planning

Start early! The best time to prepare for a business transfer isn’t when you’re ready to retire; it’s well before that. Outlining a succession plan early allows for a gradual and more effective transfer, which can take years, not just days. It also provides a clear pathway for potential successors to follow, ensuring they are ready for their new roles.

Define Your Vision for the Future

What do you see in your business’s future? Your vision for the company’s path forward should guide the succession plan. Having a clear direction will help you identify the right person who can drive that vision forward, aligning their skills and ambition with the business’s long-term goals.

Identify Potential Successors

Look around you. Who has the potential to lead? Sometimes, a family member is ready to take over; other times, an employee shows exceptional leadership skills. In some cases, an external candidate might be the best fit. Evaluate the capabilities, experience, and dedication of all potential candidates before making this critical decision.

Develop Leadership Skills in Candidates

Just spotting talent isn’t enough. Nurturing it is key. Provide potential successors with opportunities to grow and lead within the business. This could mean giving them new projects, involving them in strategic decision-making, or providing leadership training. Real-world experience is one of the best ways to prepare someone for the top job.

Seek Professional Advice

Getting advice from legal, financial, and business advisors is crucial. They can provide insights on the implications of ownership transfer, including taxes and estate planning. Their expertise can help avoid common pitfalls and ensure a successful and legal transfer of power.

Communicate with Stakeholders

Talk to your team. Openly communicating with your employees, customers, suppliers, and other stakeholders about your succession plan can build trust and minimize uncertainty. Keeping stakeholders informed can help maintain business operations without disruption during the transition.

Create a Formal Succession Plan

Documentation is important. A written plan that outlines the succession process can be a valuable roadmap. It should detail the timeline, training process for successors, and how you will handle the transfer of responsibilities and ownership.

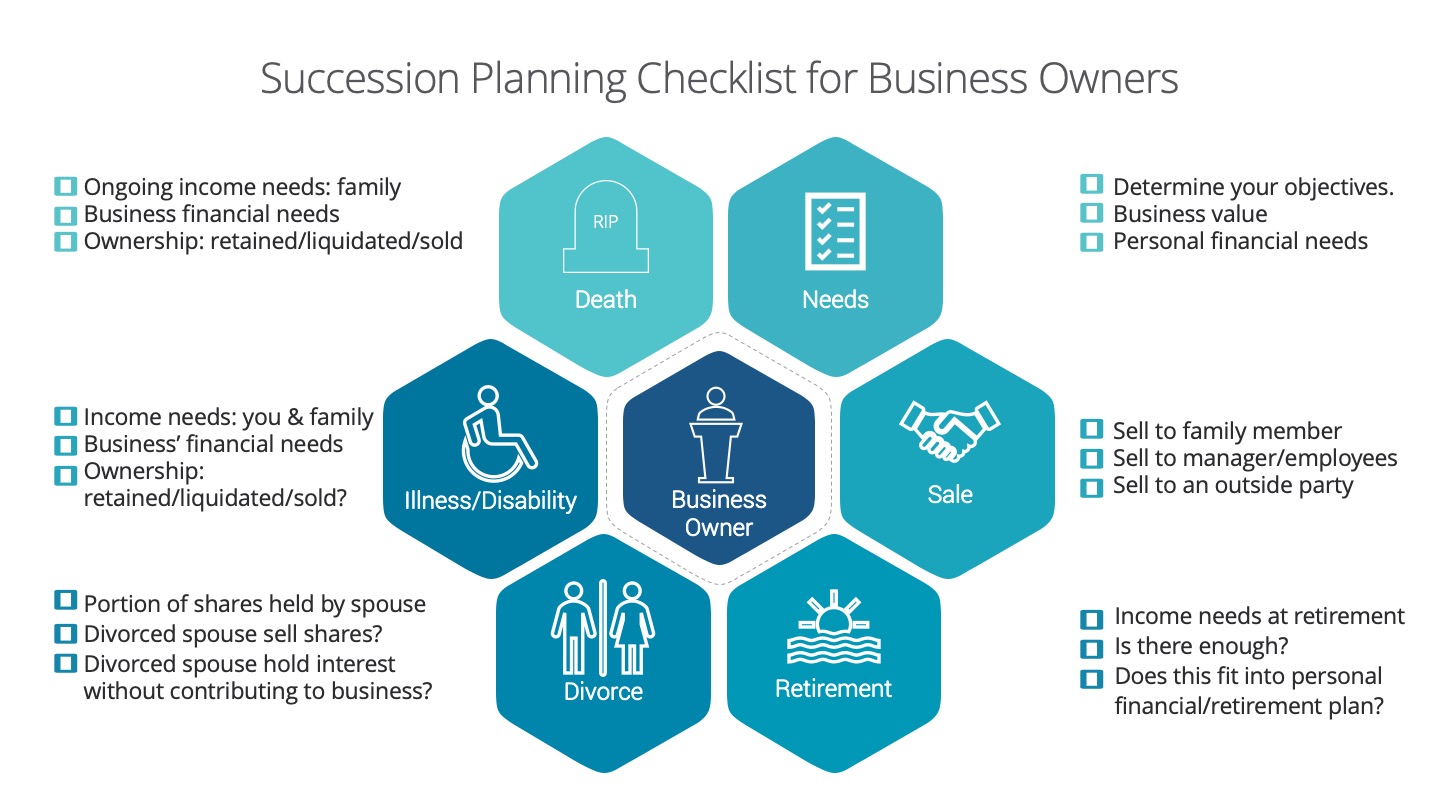

Planning for the Financial Aspect of Succession

Money matters. Considering how ownership transfer will affect your financial situation is essential. This means understanding how the transition will impact your retirement, the valuation of the business, buy-sell agreements if there are multiple owners, and how the purchase will be funded.

Consider the Emotional Impact

Let’s talk feelings. Transferring your business to someone else can be an emotional experience, especially if it’s a family business. Be prepared to manage your emotions and those of others involved in the transition. Having clear, rational reasons for choosing your successor can help smooth over any emotional ripples.

Incorporate Flexibility into the Plan

Be ready to adapt. Unforeseen circumstances can arise, and it’s vital to build flexibility into your succession plan so it can adjust to changes. This could mean cross-training multiple candidates or having interim leadership solutions in place.

Ensuring a Smooth Transfer of Knowledge

Knowledge is power. Ensure the successor has all the necessary information to run the business effectively. This may involve in-depth training or creating comprehensive manuals that capture the knowledge of the current leadership.

Set a Timeline for the Transition

Timing is everything. Too fast and the successor may not be ready; too slow and the business could lose momentum. Setting a realistic and clear timeline for the transfer helps keep the succession on track.

Execute the Succession Plan

When the time comes, put the plan into action. This might involve gradually shifting responsibilities to the successor, starting with less critical tasks before moving to more essential roles. Regular assessment and feedback during this phase can ensure any issues are promptly addressed.

Foster a Supportive Environment

Support from a team can make a big difference. Encourage employees to support the new leadership. This will help the successor gain confidence and authority in their new role.

Prepare for Your Next Chapter

It’s not just about the business. Consider what you will do after transferring ownership. Planning for your future, whether it involves retirement, new business ventures, or another passion, is an important part of the succession process.

Regularly Review and Update Your Succession Plan

Times change; plans should too. As your business evolves, so should your succession plan. Regularly reviewing and updating it ensures that it remains relevant and effective.

In conclusion, transferring business ownership is a multifaceted process that demands thoughtful planning and strategy. By starting early, choosing the right successor, preparing them for leadership, communicating effectively, and executing the plan with precision, your business can maintain its legacy and continue thriving into the next generation. Remember, a smooth succession doesn’t just happen; it’s the result of careful preparation and a commitment to sustaining the business you’ve worked so hard to build.